Do The G7 Enjoy Exorbitant Privilege?

And Why The US Has Reached The End Of The Road

Being an economist means having a huge amount of reading that you will never get through. I currently have 205 PDFs open on my laptop, which apparently I am going to read.

Besides the huge volume, getting through this reading is extra-impossible because sometimes you read one thing, and it causes you to download another 10 PDFs.

Or, you read something that pushes you to spend 3 hours looking through data, as it has got your creative juices flowing.

This is what happened when I read this excellent note from the Peterson Institute:

In this note, Rogoff and Tashiro assess whether Japan still enjoys exorbitant privilege, and their method was both intuitive and remarkably simple.

Rather than stick to my plan of reading 10-15 of those PDFs, I allowed myself to spend a few hours diving through data.

I wanted to answer the question of whether exorbitant privilege existed across the G7.

And here we are, rather than ticking 10-15 PDFs off my list, we have this blog post, where we answer that question.

But first, let’s take a step back.

What Exactly Is Exorbitant Privilege?

Back when it was coined in the 1960s by French Finance Minister Valéry Giscard d’Estaing, “exorbitant privilege” was a phrase to describe the “asymmetric financial system” with the US dollar at its centre.

With most currencies pegged to the dollar, and the dollar pegged to gold, the US had unique advantages. It was able to run persistent current account deficits (other countries faced greater constraints), while demand for dollar assets depressed US financing costs, and it did not face the same balance of payments risks as other countries. The system was seen in France as exchanging real world wealth for paper claims on the US.

Subsequently, France, having had enough with this system, began to take advantage of the convertibility of dollars into gold (i.e. asking the US for gold in return for its dollars at the pegged rate). The issue here was that the US had far too little gold to convert all the dollars into the metal.

This situation culminated in Nixon ending gold convertibility in 1971, which also ended exorbitant privilege in its initial form. However, even after 1971, the US remained central to the global financial system, and enjoyed major perks for being so. Exorbitant privilege remained.

So what exactly is exorbitant privilege?

Put simply, it is the ability for a country to pay a lower yield on its international liabilities than it earns on its international assets, embedding persistent positive returns on international investment. This comes due to structural demand from overseas investors for financial claims on the county, even if those are low yielding.

This structural demand might be due to high global usage of the currency, for instance in central bank reserves (see chart below from Rogoff and Tashiro), international debt, or in trade invoicing. A stable policymaking environment, credible monetary policy, solid macro fundamentals, a strong legal system, political stability, and deep and liquid financial markets all lend themselves to increasing international usage of the currency, which could drive exorbitant privilege.

Do The G7 Enjoy Exorbitant Privilege?

To be more concrete, we define the extent of exorbitant privilege in the same manner as Rogoff and Tashiro as “excess return on external assets over liabilities”

It is quite simple to calculate these variables. Income from assets and financing costs from liabilities are recorded in BOP primary income data within the current account (income is a credit, financing costs a debit). The total of international investment assets and liabilities are both recorded in international investment position (IIP) data. Then, we can find yields quite quickly:

Then for exorbitant privilege, we just find the differential between these two, and chart it. A positive figure suggests exorbitant privilege, with a higher number implying greater benefits.

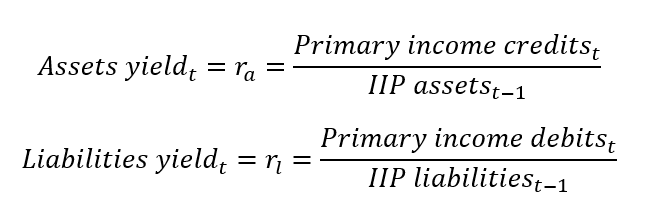

The data shows that the US and Japan maintain a very high level of exorbitant privilege, with yields on international assets persistently approaching 2pp above yields on international liabilities over recent years. Meanwhile, in spite of adhering to many of the benchmarks for encouraging international use of a currency as we mentioned in the prior section, Canada and the UK do not benefit from any sort of exorbitant privilege as we define it.

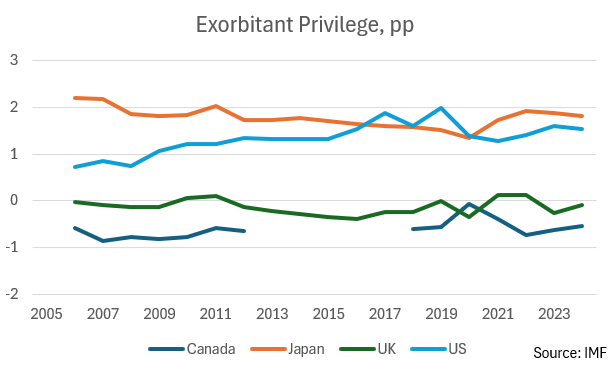

Considering the final three G7 countries, France, Germany, and Italy have typically enjoyed a modestly positive yield differential on their assets over their liabilities over the last two decades, including through the eurozone crisis. Italy is a laggard, in line with its poorer economic fundamentals and general poor macro performance. High international usage of the euro appears to have embedded a modest amount of exorbitant privilege into at least the largest eurozone markets. However, the positive yield differential is much smaller than it was for Japan and the US.

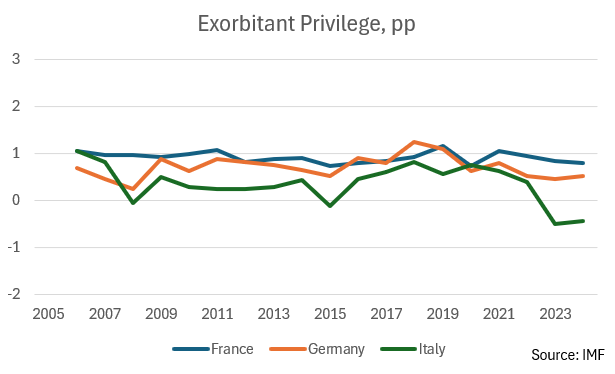

On the flipside, we can also consider a country which is known to export a significant amount of capital. We have charted below our measure of exorbitant privilege for China, which is persistently negative given China pays a higher return on its liabilities than it receives on its assets.

The US Is Reaching Its Exorbitant Limits

Exorbitant privilege can be quite powerful. For the US, it has meant that it has been able to run a persistent primary income surplus for many years in spite of rapidly growing net international investment liabilities, i.e. an increasingly negative net IIP (NIIP).

In spite of massive international accumulation of paper claims on the US, the US has not seen a significant increase in servicing costs on its international liabilities. Its degree of exorbitant privilege has withstood a remarkable cycle of leveraging.

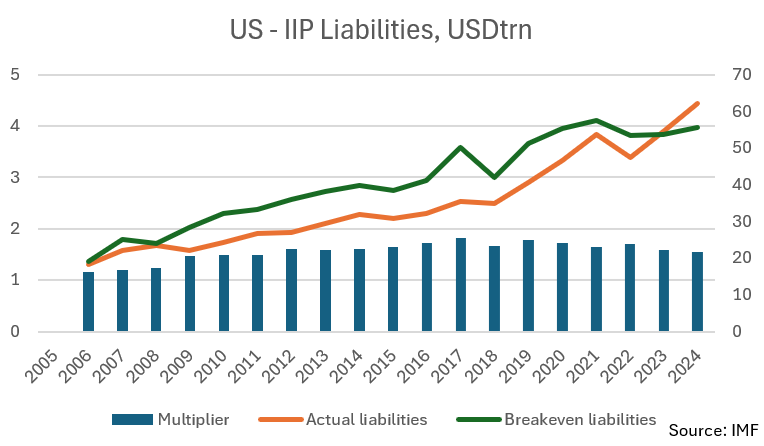

Put another way, in a practical sense, exorbitant privilege allows a country to increase its international liabilities significantly, while still earning a positive yield differential on its international net assets. To quantify this, we can define a multiplier as the ratio of the assets yield to the liabilities yield. For instance, in 2024, the yield on US IIP assets was 4.3% and the yield on US IIP liabilities was 2.7%, so our multiplier is 1.6. Provided IIP liabilities did not exceed 1.6x IIP assets, the US will earn a positive return on its IIP, i.e. will have a primary income surplus:

The chart above shows that things clearly changed in 2024 with actual liabilities pushing aggressively above the breakeven. This is consistent with rapid deterioration in the primary income balance. We can see this quite clearly in higher frequency data from FRED, charted below.

In spite of the low yield on US IIP liabilities, the net international investment position has pushed so far negative that the primary income balance has slipped into deficit. This has come as primary income payments have ballooned in line with rapidly growing IIP liabilities.

Together, this implies that while the US maintains exorbitant privilege, its international liabilities are on an unsustainable path, requiring correction. If they keep growing as they are, the primary income deficit will balloon. The US is reaching the limits of the expanded ability to run current account deficits granted to it via exorbitant privilege.

The worst case scenario would be a failure to correct course on liabilities accumulation (i.e. a failure to consolidate the current account deficit) combined with infringements on exorbitant privilege (as threats to the sanctity of US financial assets under the Trump administration may do). This would imply higher servicing costs on its liabilities, and more liabilities.

Aside: Revaluation effects

This note is pretty much done, so thanks for reading. For the nerds, here is an aside on revaluation effects, which we did not consider.

In the above, we took an “income only” approach, leaving aside revaluation effects, considering primary income movements in year t and the IIP at the end of year t-1.

However, this abstracted the fact that through the year, the country’s international assets and liabilities will revalue in line with financial markets movements. Namely, there will be local currency appreciation and depreciation of the assets and liabilities that must be reflected, and there will also be shifts in valuation due to changes in the values of currencies.

We can justifiably ignore these. The literature suggests that such movements (at least in FX) are at least partially mean reverting and are cyclical. Further, revaluation effects are a bookkeeping entry, not representing actual international flows, and if valuations normalise, may never have a real world impact. Including revaluation introduces a considerable degree of volatility into the output without obvious benefits.

Revaluation in particular distorts the US data. The decade to 2024 saw the US benefit from major financial market outperformance and a surging dollar. This generated revaluation effects that boosted the value of claims on US financial assets, while the value of US claims on the rest of the world declined.

More precisely, we estimate revaluation effects as:

i.e. we say any change in IIP assets and IIP liabilities that cannot be explained by financing flows must be due to revaluation.

Incorporating revaluation effects, we might infer a gradual erosion of privilege. However, as above, it is not clear that this is economically meaningful given revaluation effects are a bookkeeping exercise.

JB Macro is my blog, where I splurge out my brain. I’m building a following for my passion, writing about economics and markets, and it would be really great to have you on board. Please consider pressing the subscribe button below (it’s free!!). Thank you, James.

This newsletter is for informational purposes only. It does not constitute investment advice or an offer to invest. The views expressed herein are the opinions of JB Macro exclusively. Readers should conduct their own research and consult with professional advisors before making any investment decisions.