Essential Reading From May 26

All The Good Macro I Read In May 2026

In this note, I outline the noteworthy macro I read in May, with my summaries. The full reading list is updated regularly here.

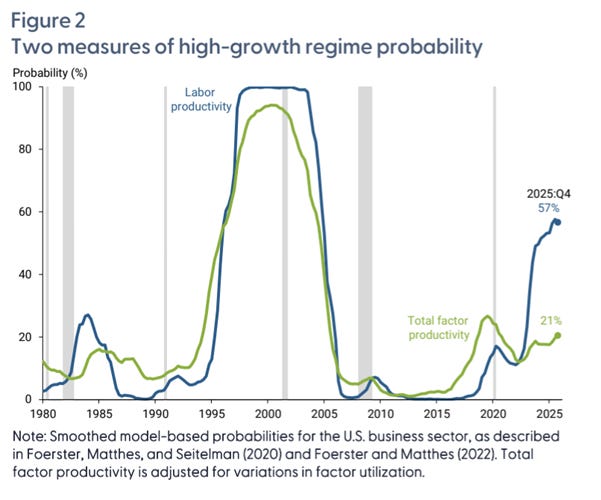

Have We Entered an Era of High Productivity Growth? San Fran Fed (note), May 2026: Using a regime switching model, analysis from the San Fran Fed assesses the likelihood that the US economy has entered a high-productivity growth regime (100% equalling definitely high productivity growth) like the late 90s/early 2000s.

The initial model found that labour productivity figures suggested a 57% chance that the economy was in a high productivity growth phase while total factor productivity (TFP) figures suggested a 21% chance. The figure for labour productivity is higher given labour productivity growth has been higher than TFP growth recently as much labour productivity growth has just reflected capital deepening (TFP assesses the productivity of both capital and labour input).

A problem with the above chart is it uses perfect hindsight.

For any given quarter, the model-based probabilities shown in Figure 2 use information from the entire sample period, which goes through 2025. In other words, when the model assesses whether the economy was in a high productivity regime in 1995, it already considers that the economy indeed experienced a surge in productivity in the late 1990s and early 2000s. This makes the computer and internet boom more obvious in retrospect than it actually was at the time.

This makes the current 57% figure look low compared to the 100% figure from earlier in the sample period.

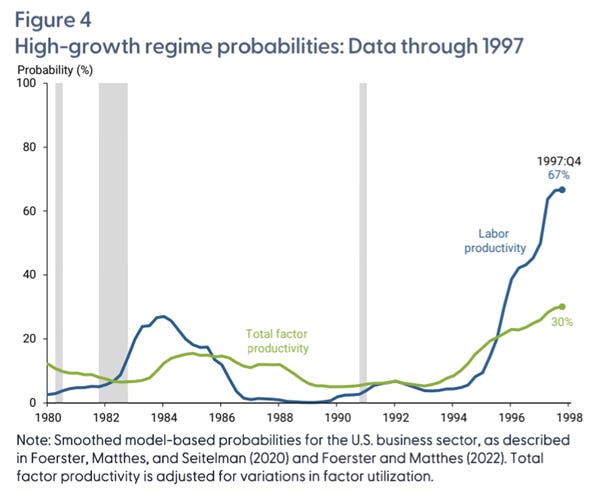

Figure 4 [below] removes the benefit of hindsight and restricts the data used for determining the regime probability to end in 1997. With this restriction, the picture is notably less clear. In 1996 and 1997, both measures showed rising probabilities, with labor productivity sending a more optimistic signal than TFP. There was no certainty that the economy had already entered a period of sustained high productivity growth. This result is compounded by the fact that our estimates use currently available data that have been revised; thus, our estimates understate the uncertainty at the time, which were based on unrevised, preliminary data estimates.

The dynamic then was similar to what we have seen in recent years. If today mirrors what we experienced in the mid-1990s, we may be in the early stages of a productivity boom driven by AI that will only become clear in retrospect.

In the 90s, labour productivity growth rises first as firms implement capital investment, then TFP growth follows. Per the chart above, we have already seen the rise in labour productivity growth on the back of capital deepening and a modest rise in TFP. If the 90s are a good guide, then high TFP growth will follow:

The Labour Party Is Playing With Fire Over Its Future and the Future of the Country – Tony Blair (essay), May 2026: We kind of hate it when Tony Blair intervenes in UK politics, as Keir Starmer no doubt does too. But his recent essay is annoyingly very good, offering a prescient diagnosis of the UK’s problems and wise recommendations to address them.

A valid criticism of this essay though is that he makes no effort at all to make the policy platform politically palpable to anyone, instead insisting that the problems are so tough that we need to grin and bear it. This is notably different from his approach during his time at the helm of the country, when New Labour made huge policy shifts firmly grounded in a narrative of fairness and shared prosperity, not pure pragmatism.

Stablecoins and the future of money: separating functions from instruments – ECB’s Lagarde (speech), May 2026: We generally agree with the analysis in President Lagarde’s speech (not a phrase we are used to saying) on the outlook for stablecoins. We remain skeptical that stablecoins will be a core pillar of the future of finance.

Lagarde:

But what this debate has not asked clearly enough is what, precisely, stablecoins are for. The benefits attributed to them rest on two distinct functions – a monetary function and a technological function that are systematically conflated in the current debate…

The argument I want to develop today is that once we disentangle those two functions, the case for promoting euro-denominated stablecoins is far weaker than it appears. And a more fundamental question comes into view: do we actually need stablecoins to obtain the benefits they are said to provide? Or are we mistaking the instrument for the outcome, when what matters is the architecture underpinning which other instruments can safely emerge?

… Euro-denominated stablecoins, operating within the framework already established by MiCAR, could generate additional global demand for euro area safe assets.

But these stablecoins need to be assessed alongside the trade-offs they would create, at least two of which are material.

The first concerns financial stability. Stablecoins are private liabilities whose stability depends on the credibility and liquidity of their backing. When confidence holds, they function as intended. But when it weakens, the demand for redemption can become sudden and self-reinforcing.

The second trade-off concerns monetary policy transmission. The ECB’s ability to maintain price stability depends on interest rate decisions reaching firms and households through the banking system. When retail deposits migrate into non-bank stablecoins and return to banks as wholesale funding, that channel narrows.

Taken together, these trade-offs are significant. They outweigh the short-term gains in financing conditions and international reach that euro-denominated stablecoins might provide. If we want to strengthen the international appeal of the euro, stablecoins are not an efficient way of doing so…

Nonetheless, the technology that stablecoins make accessible is genuinely transformative. DLT makes it possible to build shared, cross-jurisdictional financial market infrastructure from the ground up – issuance, trading and settlement on a single platform, accessible across borders without relying on a maze of legacy intermediaries. For Europe, that opportunity is especially compelling.

For that reason, the prospect of rapid dollar stablecoin uptake in European tokenised markets is a legitimate concern that risks entrenching dollar dependency at the level of settlement infrastructure itself.

The answer, however, does not lie in rejecting technology or discouraging stablecoins altogether. Instead, we must build the public infrastructure that will enable alternative instruments, such as stablecoins and other forms of tokenised money, to operate within a framework anchored by central bank money.

On its own, the stablecoin model has two structural weaknesses as a foundation for settlement.

The first is fragility. A key benefit of tokenised financial markets is atomic settlement, but that guarantee is only as strong as the instrument that serves as cash within the system.

As stablecoins can break away from their peg during times of stress, they do not confer the unconditional finality that central bank money does. [ ] At stake is the singleness of money, the principle that a unit of currency has the same value regardless of who issues it. A settlement layer built on private stablecoins risks weakening that principle.

The second is fragmentation. The promise of tokenised finance is a single, interoperable environment, but if settlement relies on stablecoins, that environment fragments across however many competing instruments the market produces. Consequently, we end up with multiple platforms and no common anchor for convertibility. A Eurosystem survey has confirmed that the absence of a widely accepted tokenised cash settlement asset has already acted as a material constraint on the adoption of tokenisation in Europe.

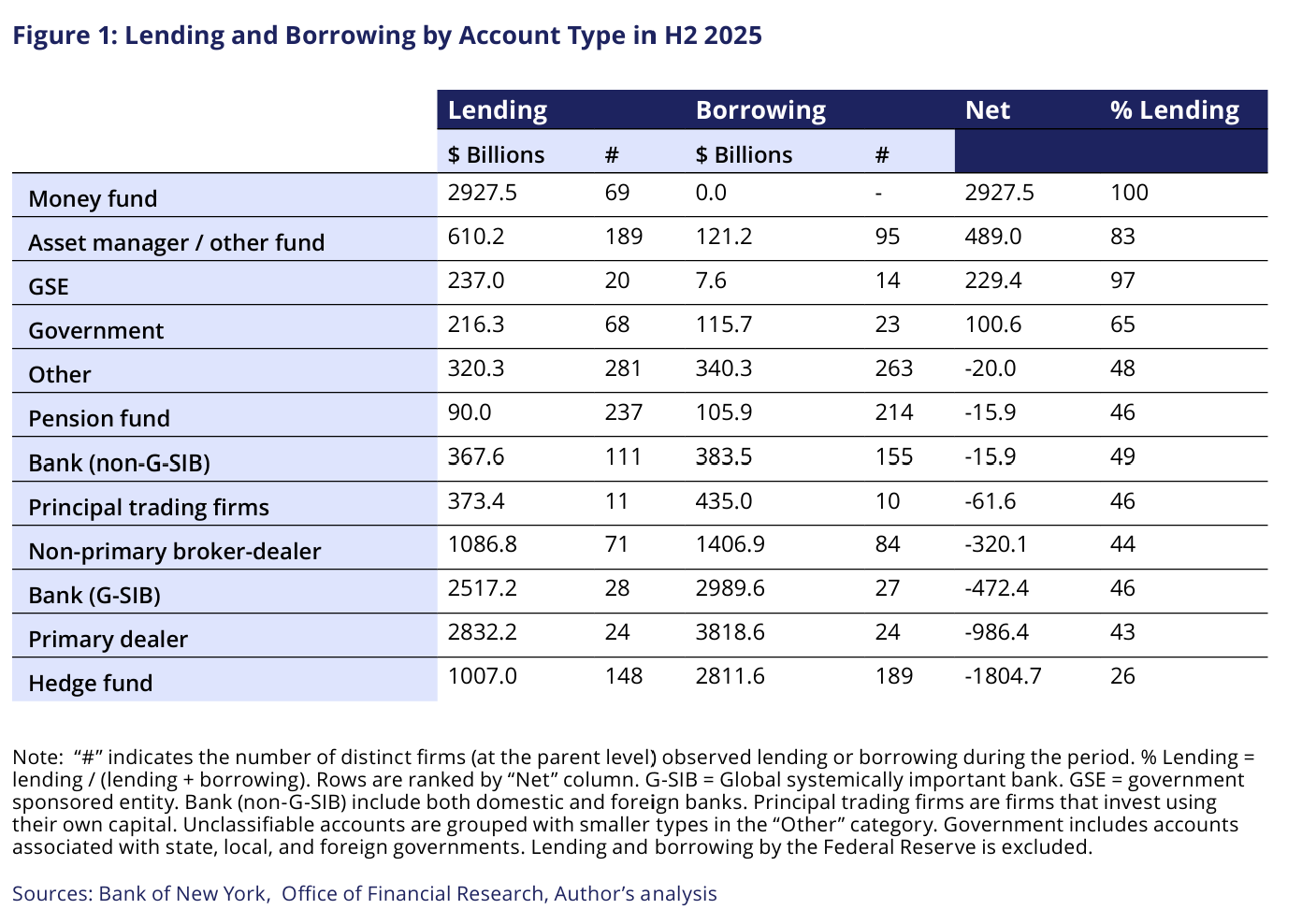

Who Participates in Repo? – OFR (brief), May 2026: Another great collection of hard to find data from the OFR. This summary of repo counterparty exposure is particularly useful:

Modernising money and markets – BoE’s Breeden (speech), May 2026: Useful summary of the BoE’s views and the focus of their efforts in the future of payments.

As technology evolves, Sarah sets out the Bank’s vision for UK finance: a robust, multi-money retail payments system that promotes greater competition and innovation, and a multi-asset, multi-currency approach to tokenising the markets of our global financial centre.

AI-Powered Algorithmic Pricing and Monetary Policy – San Francisco Fed (note), May 2026: This shift in pricing behaviour is quite cool:

The business practice of adjusting prices using algorithms powered by artificial intelligence—known as AI pricing—has grown rapidly and spread across many sectors in the economy. Unlike traditional price setting, AI pricing uses predictive analysis of large data sets to incorporate real-time changes in supply and demand conditions into pricing decisions. This enables businesses to adjust prices more quickly in response to unexpected changes in market conditions and monetary policy. Industry-level evidence suggests that price adjustments are more sensitive to monetary policy in sectors where AI pricing is more prevalent.

Banks in the Age of Stablecoins: Lessons from Their Historical Responses to Financial Innovations – Fed (note), May 2026: Previously, we have argued “if large scale adoption [of stablecoins] did happen, traditional financial institutions would respond with innovation… which would reduce deposit loss.” This note from the Fed illustrates this may happen again, in line with several historic parallels:

“banks typically respond to disintermediation threats from financial innovations not by passively accepting disintermediation, but by adapting through regulatory, product, and strategic responses. When new instruments compete with banks, whether money market funds (MMFs) in the 1970s which offered higher yields and competed for savings balances, or online payment platforms like PayPal and Venmo more recently which offered superior transaction technology and competed for payment volumes, banks initially face disintermediation pressures but historically adjust and remain active participants in the evolving financial ecosystem. Stablecoins are notable because they integrate balance-holding and payment functionality on unified digital rails and thus compete for both transaction balances and payment flows…

… Although [stablecoins] still represent a modest share of money-like instruments by outstanding value, their transaction volumes are already large and growing, and they are becoming an increasingly important competitor for transactional balances. As this competition intensifies, banks are responding with more targeted rate strategies, tokenized deposit offerings, faster and more user-friendly payment services, partnerships with stablecoin issuers, and engagement with policymakers over the future regulatory perimeter.

Importantly, history suggests that banks’ adaptation responds not just to specific innovations but to underlying structural forces. Just as MMFs reflected demand for market-rate returns and PayPal reflected demand for digital payments, stablecoins reflect demand for programmable, globally accessible digital money. Whether this demand is ultimately served by stablecoins, tokenized deposits, or other instruments, banks’ historical adaptability and enduring advantages—deposit insurance, regulatory trust, and integrated financial services—position them to remain central in the emerging digital money landscape.”

Rolling back the “big Fed” – Adam Tooze (Substack), May 2026: Excellent note summarising what we know about Warsh and what it might mean for the Fed.

Revisiting Baumol’s Disease: Structural Change, Productivity Slowdown and Income Inequality – Intereconomics (article), 2023: William Baumol derived a model of the “cost disease of services” in 1967. At the centre of this was the idea that the economy was split in two, a sector that recorded high productivity growth and one that recorded low productivity growth, with the former of these industry (or more broadly, goods production) and the latter the services. This was based on the empirical observation that services record low productivity growth while goods production recorded high.

Wage growth is set according to trends in the high productivity growth industry, consistent with empirical evidence, where the services sector essentially ends up as a labour cost price taker given a unified labour market.

Under this set up, input costs for the services continue to rise on the back of a higher wage bill, which is not offset by productivity gains. This means that cost increases are passed on to end users, pushing up services prices relative to goods prices and leads to things like education and healthcare taking up an increasing proportion of consumer spending over time, which again we see empirically.

This increased cost also means that those in the lower proportion of the income distribution may increasingly struggle to afford education and healthcare (which we see empirically, for instance in reduced access to healthcare among America’s lower earners) and may be thought of as justification as government involvement in essential services provision via progressive taxation or social insurance.

The note from Intereconomics explores the criticisms of Baumol’s disease, and suggests that the disease is still alive and kicking.

We wrote about Baumol’s growth disease and AI productivity recently, here.

JB Macro is my blog, where I splurge out my brain. I’m building a following for my passion, writing about economics and markets, and it would be really great to have you on board. Please consider pressing the subscribe button below. Thank you, James.

This newsletter is for informational purposes only. It does not constitute investment advice or an offer to invest. The views expressed herein are the opinions of JB Macro exclusively. Readers should conduct their own research and consult with professional advisors before making any investment decisions.