Upside Risks To UK Rates

Another Reason To Be Long Sterling

On this blog, we trade macro, and publish it all. We’re currently long gold and GBPCHF, both smalls as we’re easing ourselves back in after some time on the side lines. Today, we’re talking about upside risks to the UK rates outlook. Enjoy :)

Trade Idea: Long GBPXXX On A 6M Horizon

Over the last few weeks, I’ve laid out my bullish sterling medium/long term view on my expectations of upside surprises on the UK near term growth outlook, political stability, no nasty surprises in the Spring Statement, and progress on long term challenges (mainly tackling low UK productivity growth).

I’ve also separately laid out my expectations that the BoE would surprise current STIR implied Bank Rate pricing of around 65bps of rate cuts come end-2026 to the upside, taking Bank Rate down by around 125bps by the end of that year. These are somewhat messy views to hold together, and clearly there are downside risks to my sterling view should the rates view play out.

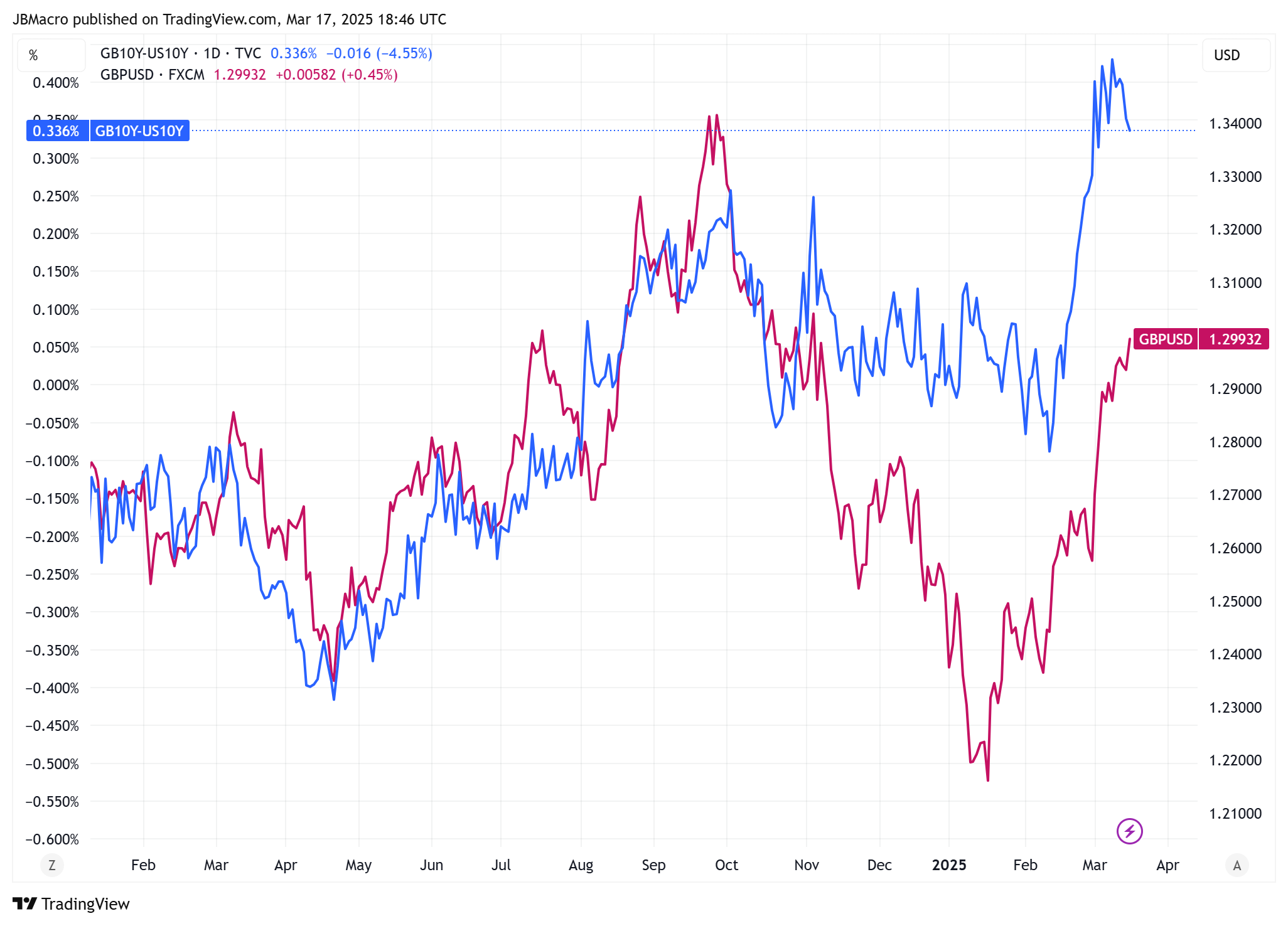

While the yield differential is a strong forecaster of the exchange rate, this is not always the case, with the Autumn Budget in late October case and point – per the chart below, there was a major up move in UK yields as the market priced higher government borrowing, which was accompanied by a big weakening in sterling. This sterling fiscal related discount remains, and I expect it to be increasingly priced out over the coming months.

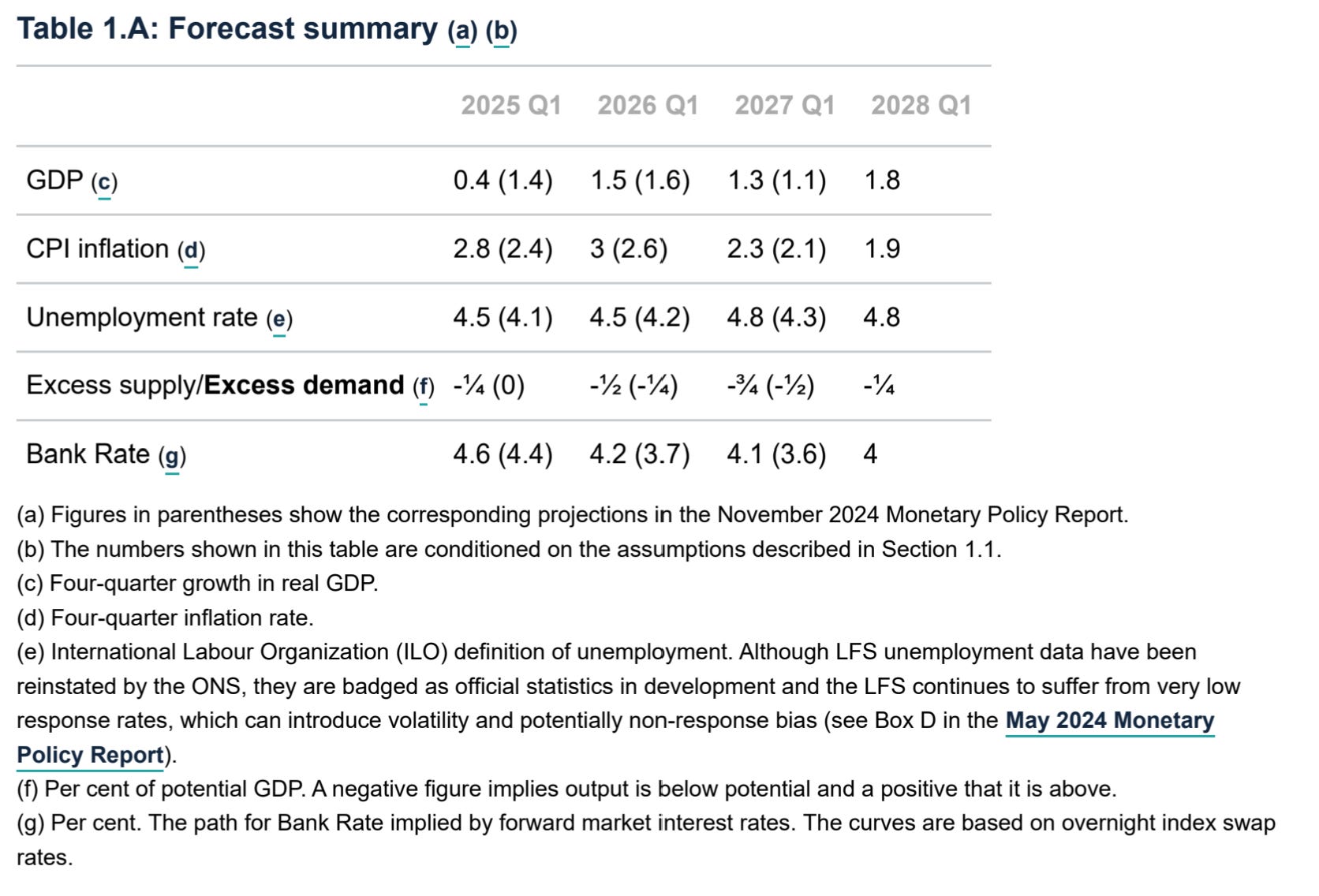

The BoE has also provided quite a nuanced outlook on the inflation and growth outlook. The February MPR detailed a higher inflation lower growth outlook, but under the surface there were considerable details and caveats. Higher inflation was largely premised around higher gas prices and jumps in April for many regulated price products (as opposed to persistent inflationary pressures that the Bank cares more about), while the labour market is now considered to be broadly balanced and not a major source of inflationary pressures. The Bank has given every indication that they would look through such a surge in inflationary pressures, with their baseline forecast of a peak of inflation in 3.7% in Q3 not dissuading some fairly dovish stances from much of the MPC.

BoE Feb 2025 MPR Forecast Table:

While the Bank materially lowered its GDP growth forecast, this shift was not accompanied by a major pickup in its forecasts for economic slack (excess supply over excess demand in the table above), which its commentary indicated was due to a fall in productivity growth. MPC members have noted that productivity growth has been unusually low over the last couple of years, and is unlikely to remain so low. That said, a supply side driven upside surprise in growth could still be accompanied by lower rates.

So we have a somewhat complicated view, of higher GBPXXX but with pullbacks as lower rates are priced. However, recent data has given my pause for thought on my rate views. That is not to say I am not maintaining my core view, but I am now carefully watching the incoming data with mind to adjust it.

Some MPC members (e.g. Ramsden here) have indicated that they are giving increasingly high weight to survey data given major uncertainty in the economic data, not least the well documented issues in the labour force survey.

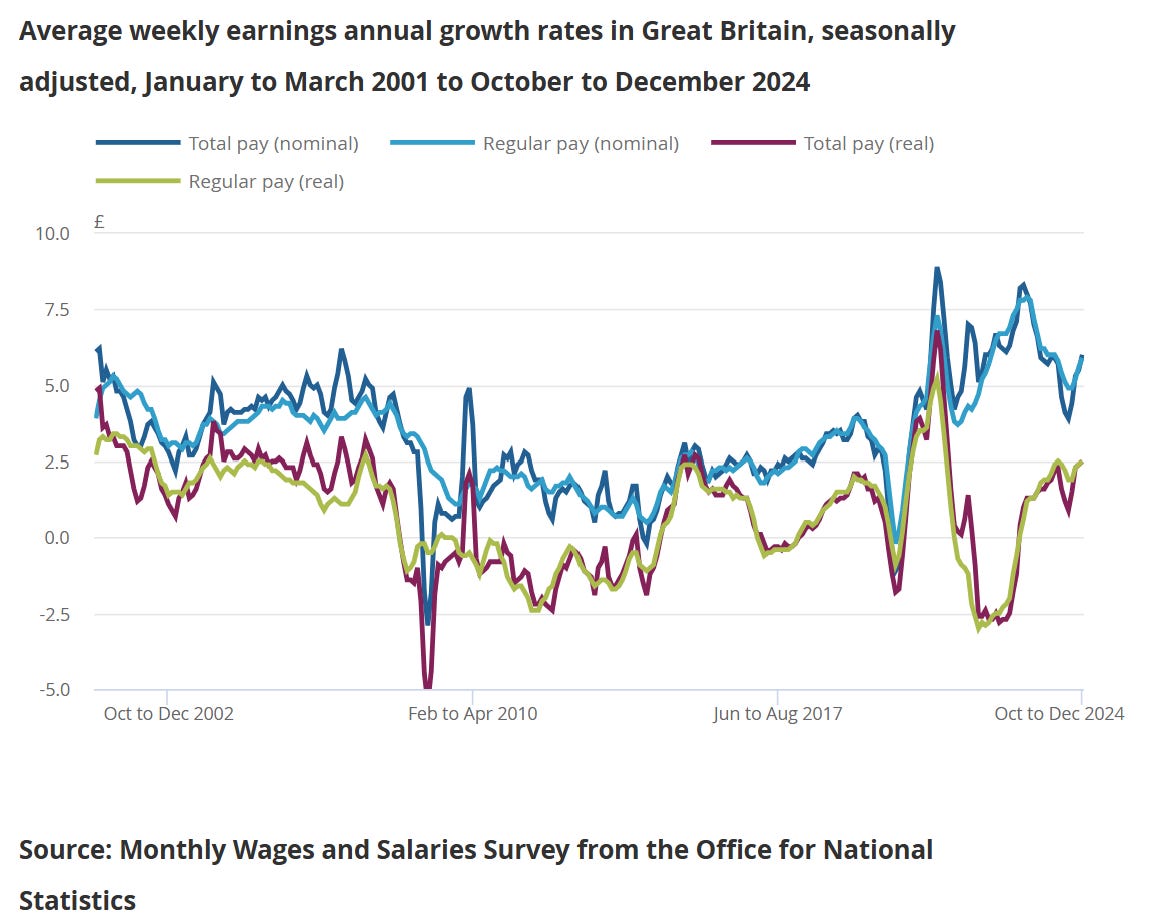

Following some upside surprises in the AWE total pay growth into late 2024 (wage gains at 6.0% y-o-y in December, chart below from the ONS), survey data into early 2025 gives a crucial read on whether this is an unwelcome trend of even more stubborn wage growth than we currently have.

The first key survey data we got in this regard was the Bank’s 2025 Agents’ Annual Pay Survey, with surveys taken over Nov/Dec 2024. This showed expectations of pay growth settlements at 3.7% in 2025. This importantly is down from actual settlements of 5.3% in 2024 (Agents’ estimate for 2024 at the end of 2023 was 5.4% - they’re quite good forecasters).

However, the November 2024 MPR estimated wage growth in the 2.0-4.0% region for 2025, so this figure is at the top end of that forecast, and importantly, wage growth at 3.7% would be above inflation target consistent wage gains of around 3.0% y-o-y (2.0% inflation target + perhaps generous productivity growth of 1.0%).

I could fairly comfortably look through the rise in AWE wage growth into end-2024 and the still elevated Agents’ pay survey given increasing labour market slack per other sources, but recent data from the Bank’s monthly Decision Maker Panel (DMP) also shows a somewhat concerning trend.

DMP panel data from February (released 6 March) shows an emerging uptrend in expected price growth over the coming year to 4.0% (3MMA to Feb), up from lows of 3.5% (3MMA to Oct). At the same time, wage growth expectations for the next year have struggled to push meaningfully lower over recent months, settling at 3.9% (3MMA to Feb).

This has not been accompanied by a shift towards higher demand for labour. Expected employment growth over the next year has collapsed to 0.1% (3MMA to Feb) while the recruitment difficulties surveys show a rise in firms reporting they are not recruiting from 5.1% in Jan 24 to 7.0% in Feb 25.

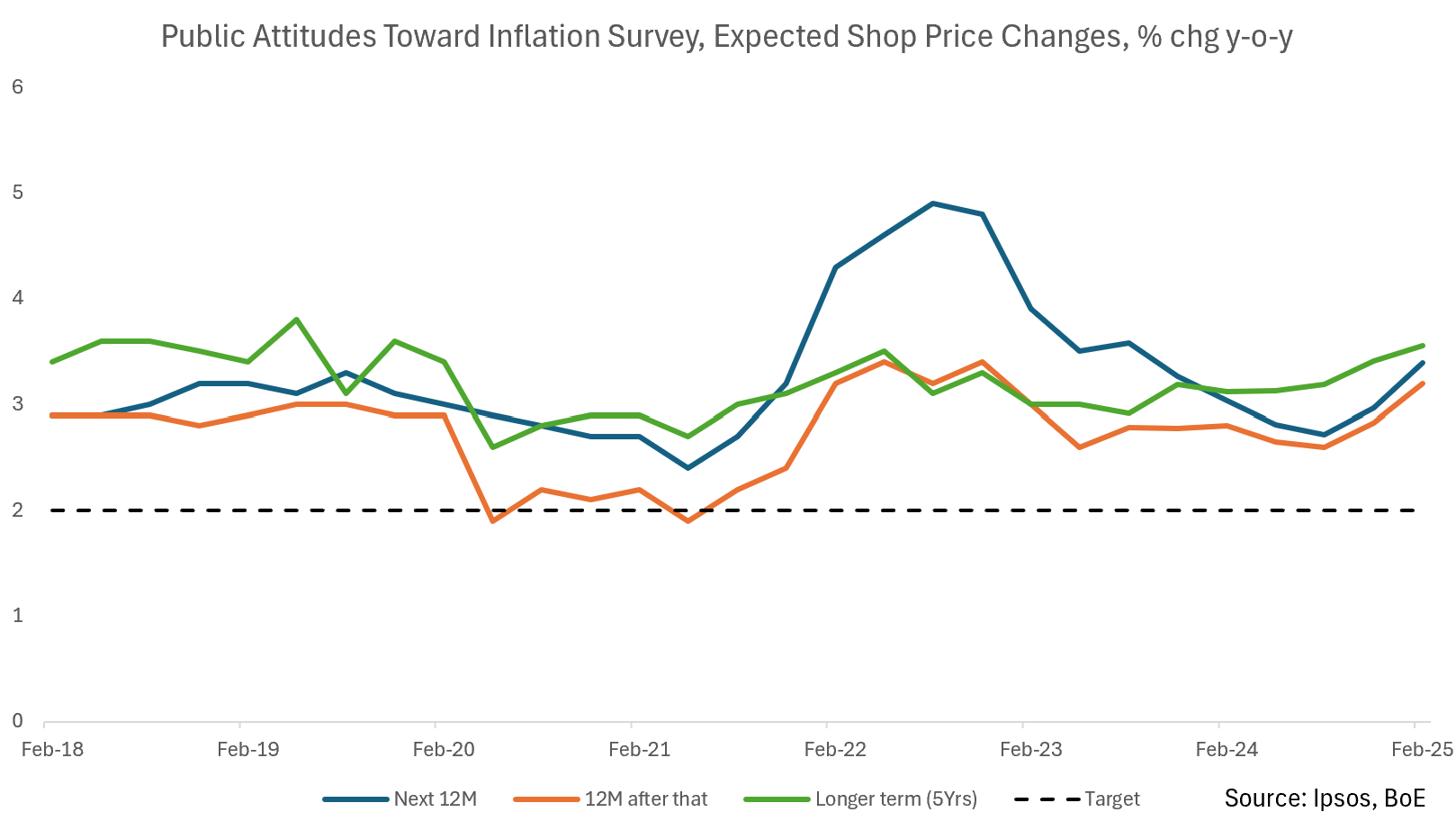

Further, the Ipsos/BoE consumer inflation expectations poll shows a similarly disconcerting trend. I’m never sure how much weight to give these, with inflation expectations typically being driven to a large extend by present inflation, and recent data not showing the sort of downside stickiness that would be of concern to policymakers. Nevertheless, the recent rise of immediate and longer term inflation expectations is not a welcome one.

These survey data raise two related prospects. First, that the disinflationary trend could be disrupted over the coming quarters, with second round effects from the jump in energy and more broader regulated prices proving sticky. Second, this could be accompanied by continued increasing labour market slack and underperforming output, possibly as productivity growth remains very low. This might indicate that something akin to stagflation could be on the cards.

Both of these would mean higher rates, with the former a clear case for stronger sterling and also reconciling quite well with our view of a strong H1 2025 for growth. The latter, I am less sure that this is a good thing for sterling given it would disrupt the long term hypothesis of rising trend growth.

In terms of which currency pair we like long sterling against, it might be tempting to look at cable and conclude the momentum behind recent up moves looks good, but IDK what to expect from the dollar here after such an aggressive recent sell-off. I think it will continue, but it could easily go the other way (e.g. on rates repricing, risk off, US risk on, etc). That’s why I’d prefer long sterling against the franc in the next six months (in line with our views from last week), or possibly a longer term relative political risk/growth play against the euro.

See ya next time :)

JB Macro is my blog, where I splurge out my brain (normally) once a week. I’m building a following for my passion, writing about economics and markets, and I would love to have you on board. Please consider pressing the subscribe button below (it’s free!!). Thank you, James.

This newsletter is for informational purposes only. It does not constitute investment advice or an offer to invest. The views expressed herein are the opinions of JB Macro exclusively. Readers should conduct their own research and consult with professional advisors before making any investment decisions.

Interesting thanks James - my sense in the re bound in GBP also helped by the rebound in stocks, though one concern for GBP maybe the fiscal squeeze to come.

BUT I would also consider funding in JPY. Lot of posts today about the jump in inflation expectations in Japan. But is that really positive for the JPY? 10 year rates at 1.5%, inflation at 2%. Unless you tell me the BOJ will aggressively hike to bring down inflation expectations… the BOJ as guilty as the rest of the global central banks. Look through inflation..

Which all also supports the bullish XAU view

One last thing - recession fears appear to be a bit overdone,

https://www.woodfordviews.com/post/calm-analysis-or-hysteria

and China appears to be helping. ‘Risk’ probably continues to be ok.